After a heady new year celebration, it’s time for US residents to put their nose to the grind and file their taxes. If you are an H1B visa holder, you are also required to follow suit, provided you qualify for the substantial presence test.

The tax filing for Indian H1B visa holders process may get tricky as do not enjoy the same benefits as US residents. Here we give you a lowdown on how to go about filing your federal taxes.

Tax Filing for Indians in the US: Who is an H1B Visa Holder?

An Indian who works in the US as a skilled professional in areas like Information technology (IT), architecture, mathematics, science, medicine, accounts, and finance qualifies for an H1B visa. And their stay is sponsored in the US by their employer for three years minimum.

Eligibility

An Indian skilled professional who has spent a minimum of 31 days in the current year and 183 days in three consecutive years is eligible under the substantial presence test (SPT). Under federal laws, they are a tax resident and are required to file federal taxes with form 1040NR.

SPT is arrived at with this simple calculation:

The total number of days present in the US in the current year + 1/3 of days present in the previous year of filing taxes + 1/6 of the number of days present two years before that.

Before we dive deep into the tax filing process for Indian H1B visa holders, let’s understand the type of taxes. The salary of an H1B visa holder is subject to Federal, state, and local taxes. They have to pay anywhere between 20% to 40% as taxes depending on their income level and deductions. Plus, they also have to pay property tax, sales tax, gas tax, capital gains tax, inheritance tax, etc.

A tax resident is liable to pay the same kind of taxes but does not enjoy certain deductions like permanent and US residents. If you become a US resident, you do get these benefits, but then your worldwide income is also taxed.

Tax Breakup for Indian H1B Visa Holders

FICA

Under FICA (Federal Insurance Contributions Act), the tax resident has to pay around 8% of his gross salary. Around 1.45% of this deduction goes for medicare while 6.2% is for social security. An equal amount is contributed by his employer. They enjoy the benefits accrued from these deductions post-retirement.

State tax

The H1B visa holder has to pay 0-10% of their salary as state tax depending on the state they live in. For instance, Alaska, Nevada, Wyoming, Washington, Florida, South Dakota do not levy a separate state income tax. And Tennessee and New Hampshire only charge taxes on interests and dividends earned by him. While California asks employers to deduct 7% of the gross salary as state tax.

Moreover, in certain states, the amount deducted as social security is returned to the employee once they leave the country. This depends on the agreement that the state has with the federal government.

Local taxes

The ex-pats from India also have to pay local taxes on their gross income which amounts to around 4%.

Once you have scored positive in the SPT, you require the following documents to file your tax returns:

Photo identity card

Social security number

Wage documents and salary statements from the employer

Investment income statement

Other income statements

Forms W-2 and 1099 series

Receipts to back up deduction claims

Documents related to the name change, dependency, in case of marriage of married individuals.

If you have a dependent, you have to use the 1040 NR form to claim deductions.

Who is a Dependent?

Any person – parents, relative, children – who live with the H1B visa holder is termed as a dependent. They have to apply for an H4 visa and cannot take up employment. But are allowed to study in the US. A spouse with an H4 visa is not counted as a dependent.

This person also has to file taxes which they can either do jointly or together with the ex-pat. If it’s a joint application, then the H1B visa holder gets to enjoy a greater amount of deduction.

Deductions, exemptions, and tax credits

The tax structure is different for single and married individuals in the US. Married people also get to enjoy certain deductions, exemptions, and tax credits which saves them money. They have to provide receipts to avail of these benefits. Now let us look at this one by one.

1) Deductions: The H1B visa holder has to file under Schedule A of form 1040 to claim certain deductions like US residents. They get to avail deductions on state and local taxes, interest on a home mortgage, dental and health expenses, losses on account of theft, casualty, and others. They need to itemize these in the claim form.

2) Exemption: Unlike US residents, the visa holder does not get exemption on dependents. However, they can request certain exemptions for themselves and their spouse if they are filing taxes separately.

3) Additional tax credits: The H1B visa holder gets limited deductions and exemptions but has respite in the form of tax credits. Some of these include child tax credit, dependent credit, adoption tax, education credit, earned income credit, etc.

After filing your taxes you have to wait for six to eight weeks to get your tax refunds. The IRS (Internal Revenue Services) clears the refund within 21 days of accepting the e-file of tax returns.

If you have adhered to the above points, filing your taxes in the US will be a smooth process. Filing taxes can be cumbersome if you are unaware of the US taxation laws. If you are an H1B visa holder working in the US, contact us to help you file your e-tax returns on time. With over 15 years of experience in this field, backed by efficient accountants, we have helped over 2 lac Indians file their taxes to date.

A rampant virus, skeleton staff, ongoing legislative changes, and flailing funding all make for a decidedly bumpy tax season ahead. The Internal Revenue Service (IRS) is battling backlogs with a grossly understaffed team (20,000 fewer employees than in 2010) and the delays and complexities engendered by stimulus check deliveries and advances in Child Tax Credits.

President Biden’s Build Back Better plan faces gridlock in the Senate, only making matters worse. As a result, taxpayers are in for a world of frustration, and the IRS urges attentiveness in cases of tax-related documents.

More specifically, the department counsels are looking out for W-2, 1099 forms, and additional letters regarding Child Tax Credits and Economic Impact Paymentsfor those who received benefits last year.

Read on to know more about precisely what you can expect during the upcoming tax season: key dates, important information, and tips to help you prepare better.

Important IRS Dates for 2022 to Keep a Tab On

February 15—deadline for eligible employees to submit W-4 forms (tax exemption) to employers.

April 1—Deadline for Required Minimum Distribution (RMD) payments from retirement accounts for senior citizens who turned 72 in 2021.

April 18—Deadline for tax filing for most Americans.

April 19—Tax filing deadline for taxpayers in Maine and Massachusetts due to Patriots’ Day falls on April 18 in those states.

May 16—Deadline for tax filing submissions for victims of the Colorado wildfires and Midwest Tornados.

June 15—Tax filing deadline for those applying for extensions, military members, and Americans living overseas.

October 17—Deadline for taxpayers who requested an extension for tax filing submissions.

December 31—RMD contribution deadlines for those 73 and older.

Typically, the deadline to file and pay taxes is April 15; however, the dates have been adjusted due to the public holidays. With Emancipation Day falling on the 15th, the deadline has been extended to April 18. A similar occurrence is visible in Maine and Massachusetts due to Patriots’ Day on April 18.

Things to Keep in Mind While Filing Tax in 2022

As you prepare to file taxes for 2022, we recommend keeping the following in mind:

On a grassroots level, individuals may owe more to the government and receive less if they did not opt-out of Child Tax Credits or didn’t include any student loan deductions. Therefore, taxpayers have been advised to brace themselves given the fluid situation.

Child Tax Credits

As discussed above, Child Tax Credits could impact your tax outlook for the year, given that Congress not only inflated the credits but also began to pay out half of the credit value in advance.

This was done through monthly installments to help struggling families quickly. Additionally, the CTC was refundable (there was no minimum income required to claim it) but fluctuated according to income levels.

Ideally, taxpayers who received the installments would receive the remaining half of the credits as a part of their tax refund, but reconciling exactly how much was paid can complicate matters.

Some may have received more than they were eligible for, and others less. For this reason, it is imperative to safeguard Letter 6419 sent to all payment receivers so that it may be verified in your tax return.

Economic Impact Payments

Stimulus checks of 1400 USD were issued to eligible receivers from March 2021 as a part of the Economic Impact Payments scheme. If you received the entirety of the payment, you need not include any information while filing your taxes.

However, those missing some payments could be eligible to claim the Recovery Rebate Credit for the same. The missing amount would be included in tax refunds. You must note, though, Letter 6475 (YourThird Economic Impact Statement) plays a crucial role in determining whether this applies to you. Much like Letter 6419, it must be given equal importance as W-2 and 1099 forms.

Extending Your Submission Deadline

While it is never advised to miss tax deadlines, those who require more time can qualify for an immediate extension by filling and submitting Form 4868.

This grants a 4-month extension, usually till October 15. However, with it being a Saturday, the final deadline is October 17. The IRS stresses that this extension is only for submitting tax returns and does not apply to payments.

If an individual owes taxes, the deadline remains April 15. Failing to pay on time results in penalty fees. Taxpayers can incur hefty charges: 5% of the amount due each month, a monthly penalty of 0.5% of the unpaid amount, 3% in accrued interest, and a maximum of 25% of what is owed.

When Can you Expect your Refund?

The IRS urges taxpayers to check thoroughly for document and numerical accuracy and to file their taxes as soon as their documentation is ready.

The agency advises filing online and opting for a direct deposit to make the process as seamless as possible for a quick return. Taxpayers who choose direct deposits could see their accounts credited within 21 days of submission by approximately mid-February.

However, refunds involving often misused credits such as the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit (CTC) will take longer due to more stringent verification processes.

Resting your laurels will not quicken or ease the process; hence compiling documents and visiting a tax planner should be top of your priority list. A non-exhaustive list of documents required are listed below:

W-2 form from your employer.

1099 form for income earned from investments.

Mortgage payment proofs.

Letter 6149 for Child Tax Credits.

Letter 6475 for Economic Impact Payments.

Receipts and bank statements for deductible expenses.

Proofs of taxable transactions and investments for things such as cryptocurrency and Non-Fungible Tokens (NFTs).

As an Indian in unfamiliar territory, preparing to file your taxes can be a daunting task. AOTAX has been helping Indian professionals in the US with their tax requirements for almost two decades and provides hassle-free consultancy, planning, and filing services. So, sign up for free today and let us help you with financial peace of mind.

Taxes received from citizens are a country’s principal source of revenue. In India, too, the income tax collected accounts for most government revenue.

If you’re an Indian IT professional having links to the US, you may be required to pay income taxes in the United States even if you are not a U.S. citizen. Whether you should file a tax return in the United States is determined by whether the US government deems you a “tax resident.”

Although paying taxes in both countries is sometimes necessary, the two nations have treaties to safeguard NRIs, such as the Double Taxation Avoidance Agreement. Tax planning for Indian IT professionals need not be tricky when you know the nitty-gritty of the same.

Immigration and Taxes: Who Has to Pay Taxes?

In terms of taxes, the United States divides people into two categories: tax residents and non-tax residents. You may be asking how to figure out how immigration and taxes apply to you if you have recently immigrated to the United States?

Even if you are not a US citizen, you may be obligated to pay US taxes in different circumstances. Whether you must file and pay taxes is determined by the government’s classification of you as a tax resident.

However, not all non-immigrant visa holders are tax residents, though. Even if you are not a tax resident, filing an income tax return if you have worked for an employer who withholds taxes from your salary is a good idea since you may be eligible for a refund.

Non-immigrant visa holders can only become tax residents if they stay in the United States for at least 183 days in the current year. For example, if you spend 200 days in the US and have a non-immigrant visa, you must report your earnings to the Internal Revenue Service (IRS).

Furthermore, even if you spent less than 183 days in the United States during the current year, a weighted system could classify you as a tax resident.

Unless you spent less than 30 days in the United States during the current year, you are a tax resident if you have spent at least 183 “weighted” days in the US during the previous 3 years.

This means that if an NRI works in the United States and earns money from India, he is only liable for US taxes. For this purpose, the person must present a US IRS-issued Tax Residency Certificate to his Indian payee. If taxes were deducted in India, the NRI could file a tax claim in the United States for that amount.

NRIs’ income received in India is taxed differently in the United States, depending on their taxation policies. The following are the criteria on which NRI taxation in the United States may be imposed. This can help in tax planning for Indian IT professionals.

1. Income from salary

In India, if an individual receives a pay package with multiple components, each component is taxed separately. Individuals may also qualify for tax breaks or exemptions if they get medical reimbursements or allowances.

In the United States, however, the same taxing conditions do not apply to salaries. An individual’s income is taxed regardless of how much the person earns.

The taxable components of your salary are listed on the well-known Form 16 in India. In contrast, if an individual or NRI files an ITR in the United States, all tax-free components of the pay received in India must be disclosed. At the same time, these individuals must pay taxes on those components in the United States.

NRIs must use the tax return Form 1040 to report their salary income in India. Form 1116 is used to file a tax return or claim a tax credit.

2. Freelancing and contractual income

This is applicable for NRIs who provide consulting services in the United States but earn money from India. In this case, the linked NRIs are taxed in the United States on that income. Therefore, whether the income is received in the United States or an Indian bank account, this tax must be paid.

The provisions of the DTAA, or Double Tax Avoidance Agreement, must be considered in this case.

3. Rental income

If an NRI rents an Indian property, his rental income will be taxed in the United States. Any rental income from immovable property may be taxed in the country where the property is located, according to Article 6 of the DTAA.

As a result, any income from rent in India is subject to taxation for US NRIs. NRIs, on the other hand, must declare this income while submitting their US tax return. Taxes paid in India would be credited to them.

It’s worth noting that salary and contractual income are only taxed in the country where they’re earned. Both countries, however, have the option of taxing rental revenue.

The first right belongs to the country in which the property is located. As a result, the NRI will pay tax on his rental income in India first, according to his available Indian tax slab.

The rental income must then be declared by the NRI taxpayer in the United States. The tax on his entire income is then calculated using his tax bracket in the United States. The NRI might claim a tax credit in the United States for whatever taxes he paid in India.

NRIs in the United States must file Form 1040 Schedule E for tax purposes. In India, rental income is subject to a 30% tax reduction. Actual expenses, such as maintenance and repair, are deducted in the United States. Form 1116 tax credit claims must be completed.

4. Income from the sale of agricultural land

In India, the selling of agricultural land is a tax-free transaction. It is, however, taxed in the United States. An NRI’s income from the sale of agricultural property must be declared in the United States and taxed as part of their global income.

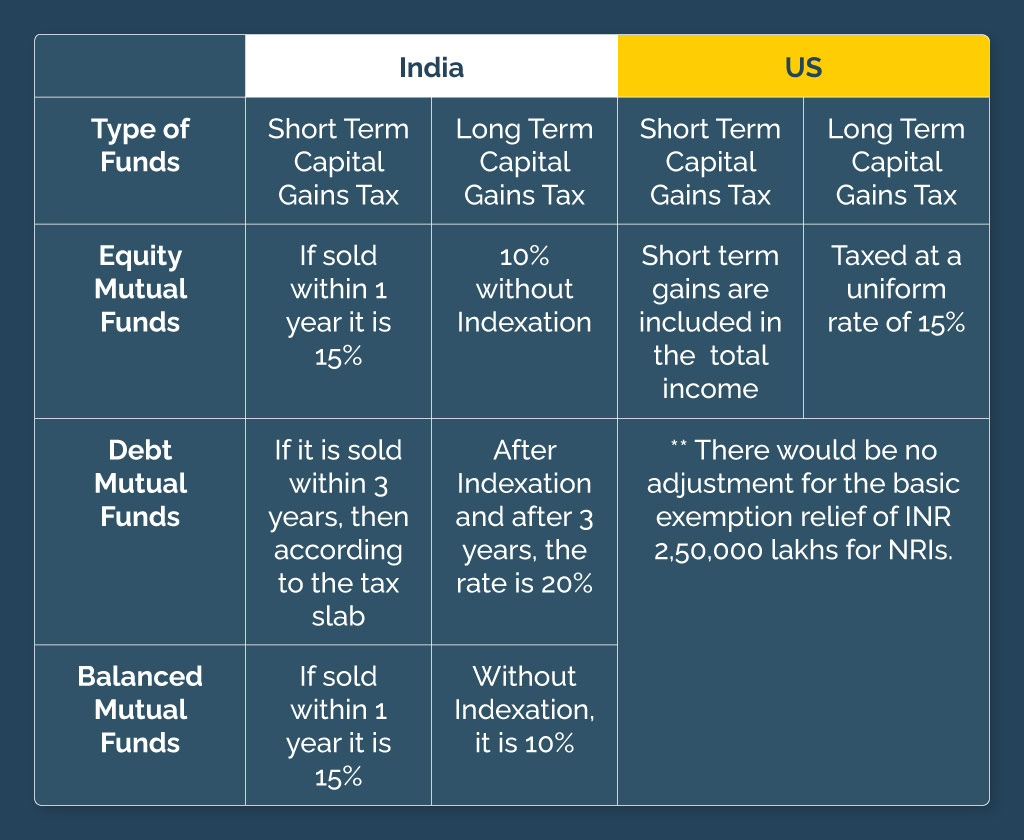

5. Capital gains

A capital gain is any profit earned from selling capital assets such as land, property, stocks, shares, mutual funds, etc. In India and the United States, the time period used to establish whether an asset is a long-term or short-term capital gain is different. NRIs face new challenges because of this.

It may result in NRIs paying tax on their sales in India and additional tax on the remaining amount in the US, notwithstanding the possibility of claiming the tax credit in the US. To an NRI, this could result in a double taxable asset.

Long-term capital gains in the United States are taxed at the same rate for all assets, one year. Long-term capital gains are taxed at a rate of 15%, whereas short-term gains are added to your total income.

The following table summarizes the above topic of capital gains taxes:

6. Income from interest generated

Interest income is added to the total income of each Indian resident and then taxed according to the overall tax bracket. This is usually 30% percent of the interest income.

Interest earned in India or the United States is added to the NRI’s total income and taxed according to the bracket in which it falls. This may be different in the United States, depending on the state’s legislation where the NRI resides.

If an NRI earns interest on deposits in India, he will have a tax deduction of TDS in India at a reduced 15 percent rate if the DTAA is in place.

7. Income from dividends

In India, any dividend income is tax-free. On the other hand, Dividends are added to total income and taxed in the United States.

NRIs must report “Interest and dividends” income on Schedule B of Form 1040 to be taxed. Foreign tax credits can be claimed using Form 1116.

8. Foreign Tax Credit Limit in the USA

In the United States, NRIs can claim a tax credit; however, the IRS has set a limit. For this, you’ll need to fill out Form 1116. This means that the foreign tax credit should be calculated in accordance with the NRI’s US tax due in the same proportion as the NRI’s total income.

It’s important to realize that taxes in the United States differ from state to state. As a result, the taxes paid by NRIs in different states vary. The above criteria for NRI taxation can help in tax planning for Indian IT professionals.

Personal tax returns can be a stressful undertaking. AOTAX can relieve you of this burden by preparing your Personal Tax Returns for you.

We are all Registered Tax Agents with vast hands-on expertise, and we all take great pride in assisting our clients in achieving their objectives.

We do everything we can to minimize your tax while making the overall taxing procedure as efficient, easy, and cost-effective as possible, thanks to a staff of highly skilled and experienced Tax Accountants. Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

It’s that time of the year when most Indians residing in the US are searching for whether and how to file tax returns online. The first question – do you even have to file taxes – is easy. The answer is yes, probably even if you are not a U.S. citizen.

If the government considers you a US tax resident (more on this later), then you have to report all income earned to the IRS and pay taxes. However, that does not automatically mean that your income will be taxable. You’re simply reporting it to the United States government.

The second question – how to file tax returns – is trickier. So, here’s a cheat sheet that tells you all you need to know about filing returns.

How to File Tax Returns Online for 2022?

The tax season begins on Monday, January 24, 2022. From that date, all permanent residents and tax residents can start filing their taxes. Also, even if you aren’t considered a tax resident, it is a smart idea to file them anyway. Why? You might qualify for a tax credit or be able to claim a refund.

Do green cardholders have to pay taxes?

Yes, all green card holders are US tax residents. They need to report all income and pay taxes, whether earned in the US or internationally. You must file tax returns using the IRS Form 1040 by April 15, 2022, even if you haven’t stayed in the US all year.

What about nonimmigrant visa holders?

If you’re in the US on a nonimmigrant visa, you may have to file taxes, depending on whether you’ve passed the Substantial Presence Test (SPT). The test declares that a nonimmigrant visa holder who has spent 31 or more days in the US in the current year is a tax resident.

You’re also a tax resident if you spend 183 days (calculated using a weight system) in “the current year and the two years immediately before that.”

As green card holders, all nonimmigrant visa holders use IRS Form 1040 to file taxes, and they have to do it by April 15th. The difference is that they only report income earned in the US. No taxes need to be paid for earnings outside the country.

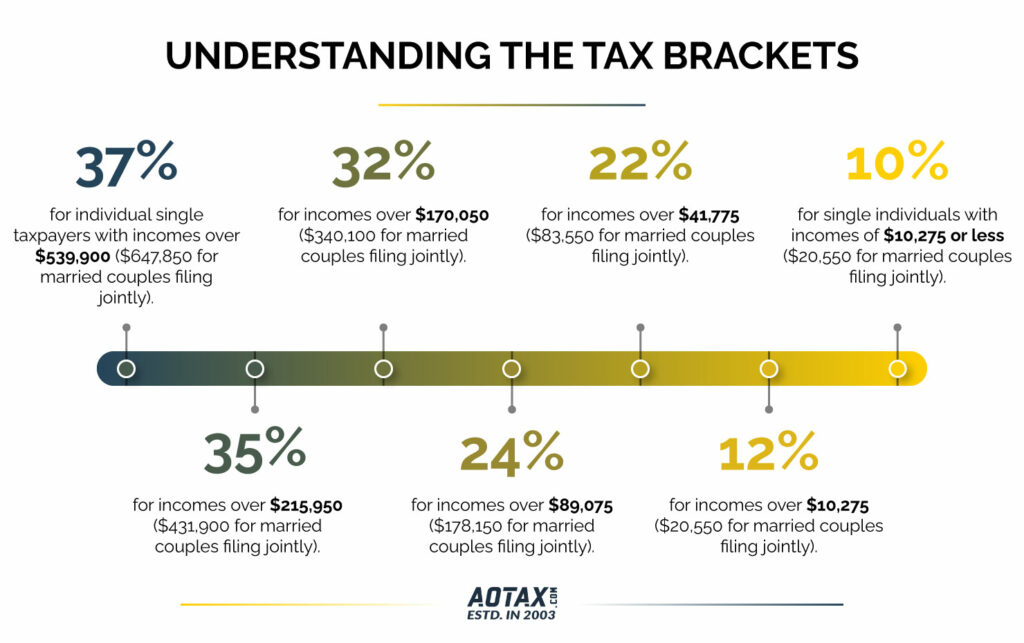

The US government uses a progressive tax system, so people with lower taxable income pay fewer taxes, and those with higher income pay more. So, how does the US calculate how much tax you need to pay? By dividing your income into tax brackets. Each bracket has its corresponding tax rate, and for this year, it is:

37% for individual single taxpayers with incomes over 539,900 ($647,850 for married couples filing jointly).

35%, for incomes over $215,950 ($431,900 for married couples filing jointly).

32% for incomes over $170,050 ($340,100 for married couples filing jointly).

24% for incomes over $89,075 ($178,150 for married couples filing jointly).

22% for incomes over $41,775 ($83,550 for married couples filing jointly).

12% for incomes over $10,275 ($20,550 for married couples filing jointly).

10% for single individuals with incomes of $10,275 or less ($20,550 for married couples filing jointly).

The benefit of a progressive system is that the tax rate does not apply to your entire income, irrespective of which bracket you fall into.

Pick how to file your tax return

You can file tax returns online, by hand, or hire a tax preparer. Filling out the Form 1040 manually and then emailing it is not a great idea because the process is much, much longer.

If you expect a refund, filing taxes online is better because the IRS processes e-filed returns faster. There is plenty of tax software that makes it very convenient.

The third option is to hire someone who provides tax preparation and filing services. You should strongly consider it if you are filing taxes for the first time, have never prepared tax returns using software, or have a complicated revenue stream. Professional guidance is crucial in the last instance.

Say you have a business that makes your finances complicated, or you also earn through a side gig, then a professional would make it easier to understand which forms are required, what common deductions to factor in, etc.

Collect all your documents

The last step before you sit down to file your tax returns online is to gather all your documents. You will need an ITIN, which is an individual taxpayer identification number. It’s issued by the IRS to people who do not have a Social Security number (SSN). You will also need to gather all:

Proof of income.

Proof of taxes already paid.

Proof of expenses to get tax credit or deductibles.

Filing taxes is never easy. But it becomes a daunting task the minute you get your provisional (and later permanent) green card. After that, you have to report all your income earned anywhere globally, even if you don’t spend a day in the US throughout the year.

For tax purposes, the US considers you their resident. It’s also a laborious task for Indians who have just gone to the US and filed their returns for the first time.

At AOTAX, we help Indians living in the US file their tax returns online. We’ve been doing this for a decade and a half with the help of an expert and qualified professionals. Besides tax preparation and filing services, we also offer tax planning advice, ITIN processing services, and extension filing. The entire process is online, making it effortless for you while ensuring you get the maximum returns possible! With AOTAX, you get to rest assured that your taxes are done right. Sign up and file tax returns online!

People often think of tax preparation when they think about doing their taxes. As tax time approaches, people scramble to find savings and frantically rush to file their returns and avoid incurring penalties. However, a tax strategy is not just for filing your taxes every year. It can be an effective means of planning for the future and minimizing your taxes simultaneously. This is exactly where you need tax planning.

So, then are tax planners different from tax preparers? In a nutshell, yes. The process of tax preparation is reactive, whereas tax planning focuses on the future.

While these words sound similar, each refers to a different aspect of taxation and has distinct meanings. As we go through each service, let’s see how they differ and choose the best one.

What is Tax Preparation?

Preparing taxes is typically a one-time task. Normally, tax preparation takes place between January and April. A tax preparer or Certified Public Accountant (CPA) prepares tax returns before the deadline for filing. Tax preparation needs several documents that provide valuable information regarding income, investments, and retirement plan statements. The approach also considers multiple income streams, deductions, and charities.

The role of a tax preparer

A tax professional prepares the tax return by organizing and entering the previous year’s tax information. So you need to visit a tax preparer once or maybe twice a year. Their expertise in tax laws ensures that returns comply with the IRS regulations. So you can rest assured about meeting the federal and state regulations.

Tax preparers can offer general tax advice and tax-saving suggestions based on your previous records. A tax preparer can address general questions regarding the filing process. There will, however, be no proactive tax strategies to help you reduce your tax liabilities. The reason – Such meticulousness, detail, and planning fall into a more comprehensive process requiring more expertise and attention.

Qualifications to look for in a Tax Preparer

Preparer tax identification numbers (PTINs) are the primary requirement for preparing taxes. A PTIN needs no additional credentials or accounting experience. Some states require tax preparation certification, similar to a PTIN but do not signify expertise or competence. Tax preparation services can be provided for a fee by qualified tax preparers.

While anyone with a PTIN and the required state credential can prepare your tax return, it’s a prerequisite to be either a Certified Public Accountant (CPA), enrolled agent, or an attorney who can address things like IRS issues, payments, audits, and collection activities.

Benefits of tax preparation

Save more money. A tax professional understands tax laws and compliance. They maximize your tax deductions and credits.

Save time. It takes a great deal of time and effort to prepare your tax return independently. A tax preparer can save all that time.

Error-free returns. A mistaken tax return can have disastrous results. Errors can lead to audits and penalties. Additionally, you can reduce your risk for audit with tax preparation.

What is Tax Planning?

A comprehensive tax strategy will help you chart a course of financial behavior that will help you manage your taxes in the future. When it comes to tax planning, it’s less about your specific return and more about how to maximize it.

The role of a tax planning agency or tax planner

Financial planning often entails a regular meeting with a financial planner and taking an active role in making decisions about your finances. Tax planning, on the other hand, is an ongoing process, one that shifts and changes as your goals do. A tax planner or tax planning agency integrates the changing financial dynamics and fosters an open and transparent relationship with its client. A tax planner will analyze your financial objectives, values, and future vision to create a personalized financial plan.

Creating a tax plan that meets your needs and considers your goals is essential. Few tax planning services like AOTAX have specific plans for businesses and individuals. They chalk out a plan considering both business and individual tax needs. The services vary from advisory services to business tax preparation and planning. All that so you can act fiscally responsible and tax-friendly.

Qualifications to look for in a Tax Planner

While tax planners require a great deal of expertise and specific knowledge, they are not subject to any federal or state regulations. They need to hold a CPA for general tax planning or be an accredited tax advisor for sophisticated cases. The biggest asset for a tax planner is their industry knowledge regarding applicable laws and particular situations.

Benefits of tax planning

Reducing tax liability. An individual tax planner or tax planning agency focuses primarily on lowering liabilities or routing investments. When you have business income, planning throughout the year ensures you maximize tax credits, harvest losses from investments, and manage your wealth accordingly.

Flexible estate planning. Don’t just leave your assets, but add a legacy to your heirs. You can lower your own and your heirs’ tax liabilities with tax planning.

Know your investment returns. Your carefully thought-out investment plan can be ruined by expenses, capital gains, and even inflation, leaving you with considerably fewer returns than you anticipated.

Tax Planner vs. Tax Preparer

Tax preparation businesses cannot provide you with the expertise you need for tax planning. Planning your taxes and saving money are two ways tax planners can help you. A tax planning strategy must be implemented year-round to minimize your tax liability.

Tax planners typically offer the following services:

Strategy for harvesting tax losses.

Tax bracket management.

Constantly plan other investment strategies which could get deserved returns while saving on taxes.

Tax preparers typically provide the following services:

File tax returns.

Comply with state and federal tax laws.

Handle missed deadlines and resolution paperwork.

Finally, a tax planning agency is the best solution by weighing the differences. A tax planner will tailor the plan to meet your needs. They care about your individual or business financial goals and plan the future. Their meticulous planning strategies will help you reach those objectives while also fitting the taxation rules. Investing and taxes can sometimes seem out of reach. But not anymore with AOTAX. Get in touch today to get your free tax draft!

Recent Comments