Top #10 most important things to know about the Economic Impact Payment Information Center

Top #10 most important things to know about the Economic Impact Payment Information Center

Under the provisions of the CARES (Coronavirus Aid, Relief and Economic Security) Act of the Federal Government, the citizens in the US have been receiving their Economic Impact Payments (EIP). The Economic Impact Payment which is being received by the Americans is calculated automatically by the IRS.

However, there are many Americans, who have several queries related to the Economic Impact Payments such as their eligibility, amount of payments, by when to expect the EIP, etc. The answers to these queries related to the Economic Impact Payments can be obtained by the common people at the Economic Impact Payment Information Center.

Some of the major things which Americans must know about the EIP Information Center can be listed below.

- Eligibility for Economic Impact payment

- Request for EIP

- Calculation of EIP

- Receipt of EIP

- Non-Filer Tool

- Social Security

- Railroad retirement

- Recipients of the Department of Veteran Affairs benefit

- Additional Information

- Return of EIP

Americans Must Know About The EIP Information Center

a.Eligibility for Economic Impact Payment

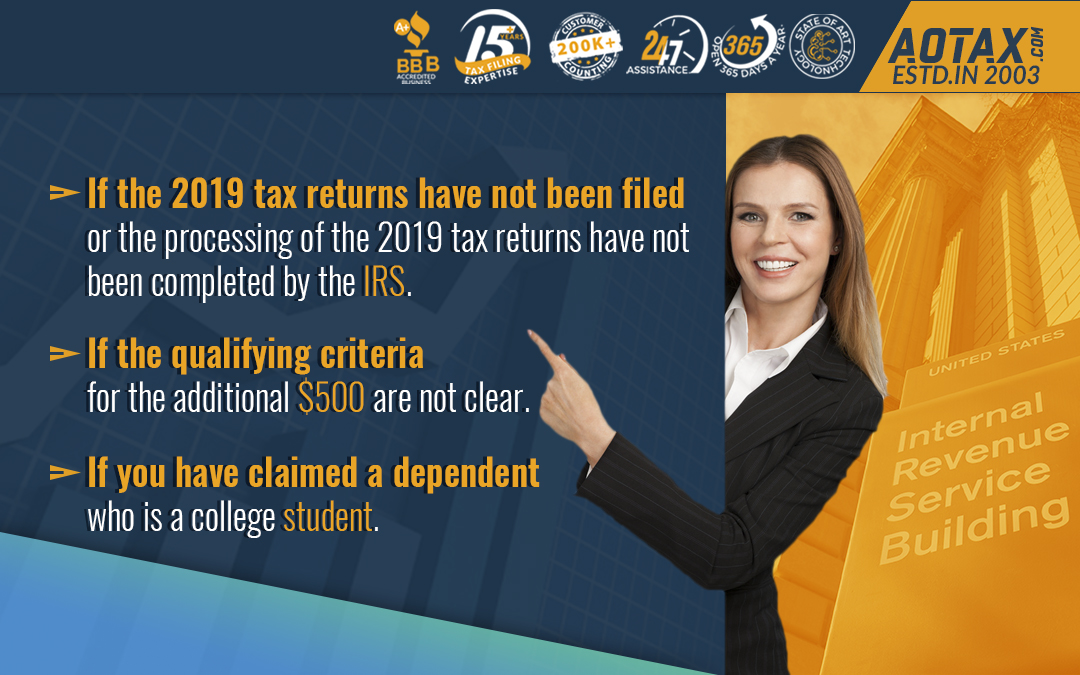

1.US citizens and US resident aliens who are filing tax returns as individuals or heads of households will be eligible for receiving EIP of $1200 whereas those who are married and are filing returns jointly would receive an EIP of $2400.

2. To receive EIP the taxpayers must not be the dependent of another taxpayer, should be having a valid Social Security Number and their AGI (Adjusted Gross Income) must be up to the given limits

- For single individuals or married couples but filing tax returns jointly, the AGI should be up to $75000.

- For those taxpayers who are filing tax returns as head of household filers, the AGI should be up to $112,500.

- For taxpayers who are married and are filing their tax returns jointly, the AGI must be up to $150,000.

3. In case, an individual does not have a valid Social Security Number, is a non-resident alien or has filed Form 1040-NR, Form 1040NR-EZ, Form 1040-PR or Form 1040-SS for the year 2019 will not be eligible to obtain the EIP.

b.Request for EIP

- If an individual has already filed the tax returns for 2018 or 2019, then there is nothing more to be done for receiving the EIP.

- The IRS would use the information of the 2019 tax returns for calculation of the EIP or would use the information of 2018 in case of non-filing of the 2019 returns.

- Taxpayers who have not filed returns for 2019 or 2018 can visit the IRS website and input their payment information in the link provided for Non-filers.

c.Calculation of EIP

- Individuals who are eligible for receiving EIP and are filing tax returns with a single status would receive $1200 as the EIP.

- If two individuals are filing their tax returns jointly, they are eligible to obtain an EIP of $2400.

- The eligible individuals would receive an additional $500 for each qualifying child who has been claimed during the filing of tax returns.

d.Receipt of EIP

- If an individual has received his tax refund for the year 2019 or the year 2018 in case of non-filing in 2019 by the method of Direct Deposit, then the IRS would use the latest information ad send your EIP by Direct Deposit.

- Moreover, in case of non-receipt of EIP through Direct Deposit the IRS would send the EIP to the mailing address present in the file of the IRS.

e.Non-filer Tool

- The Non-Filer: Enter Payment Info Here tool should be used for receiving EIP by those eligible individuals who have not filed tax returns for 2019 or 2018 and do not receive Social Security Retirement, Supplemental Security Income (SSI) or Survivor Benefits, Veteran benefits or any other benefits related to Railroad retirement.

- If you have filed your tax returns or you receive federal benefits, then the need for using the Non-filer tool is ruled out.

f.Social Security

The Social Security recipients who might not have filed tax returns for 2019 or 2018 but receive Form SSA-1099 will receive their EIP by the same method as that of the receipt of the Social Security Benefit.

g.Railroad Retirement

The recipients of Rail Road Retirement who might not have filed tax returns for 2019 or 2018 but receive the benefits by RRB-1099 will receive their EIP by the same method as that of the receipt of the Rail Road Retirement Benefit.

h.Recipients of the Department of Veteran Affairs benefit

The recipients of the Department of Veteran Affairs Benefit who might not have filed tax returns for 2019 or 2018 but receive Form SSA-1099 or RRB-1099 will receive their EIP by the same method as that of the receipt of the benefit.

i.Additional Information

Taxpayers need to be cautious about scam artists who would try to use the EIP as a strategy for performing other scams related to stealing. Taxpayers must remember that information about EIP can be obtained only by visiting the official IRS webpage and not by any calls, text, or emails.

j.Return of EIP

- For the return of EIP which was in the form of Direct Deposit, check, or money order; money order or personal check must be immediately sent to the IRS with information related to the SSN.

- If the payment was received in the form of a paper check, then it can be sent back to the appropriate section of the IRS by writing “Void” on the back of the check.

Hence, taxpayers can avoid calling up IRS for queries related to the EIP and rather visit the Economic Impact Payment Information center for resolving their queries.

Recent Comments