Is a complete understanding of the US taxation system still eluding you?

Does the complexity and endlessness of IRS forms overwhelm you?

Well, we’re here to tell you that you are not alone.

Thousands of Indian IT professionals embark to America for better pay and jobs and often get caught up in the confusing web of filing their tax returns.

A new country and different laws can complicate tax season, but you can better handle it with some preparation and organization. So we’ve come up with the ultimate checklist to help you prepare for filing your taxes.

What are the Documents Required for Income Tax Return of Individuals?

Depending on your financial and personal context, the claims you make while filing your tax returns can vary. Therefore, multiple documents are often required, which can be hard to track.

Nevertheless, we’ve categorized the documents required for income tax return of individual per the functions they serve while filing your taxes. Read on to know exactly what you need to keep handy to sail through the tax season smoothly:

Personal Information and Dependent Information

Basic identification information is mandatory while filing tax returns. Be sure to include the following documents:

Previous tax returns and statements for reference. The IRS has up to three years to decide on whether to audit an individual or not. In such a scenario, having copies of previous tax returns is necessary to ensure the best outcome.

Social Security or Tax ID numbers and dates of birth of both you and your dependents, if any. Dependents include spouses, children, parents whom you provide for financially. In the case of child dependents, furnishing childcare records is advisable.

Income-Related Documentation

Your total income determines your tax bracket and how much tax you pay. However, you are legally required to file taxes for all the types of income you receive, including rental income, interest on investments, and profits made on anything you choose to sell in the year.

In addition, the US Government taxes Indian H1B holders on their global income and their US income. Therefore, you must declare any profit-generating assets back in India as a part of your income. It is advisable to keep the documents below ready and submit them as a part of your tax return:

Form W-2: issued by your employer and states precisely how much tax was withheld from your pay.

Form 1099 series: each form in this series has a different suffix to indicate the different types of revenues possible:

1099-INT: for income in the form of interest earned on investments.

1099-G: for government payments and tax refunds.

1099-K and 1099-MISC: for payments received for freelance gigs.

1099-R: for pension income.

1099-S: for income received upon the sale of stocks.

1099-B: for income received after selling a property.

1099-DIV: for dividends received for mutual fund investments.

1099-SSA: for Social Security benefits.

Form 1040: to be used while declaring foreign income and reporting taxes paid in previous years.

Cryptocurrency transaction records of sales, if any, and interest earned.

Form 1095-A: for Health Insurance Marketplace Statements.

Rental asset records: for income earned in the form of rent.

Expense records: bank and credit card statements.

Form W-4: for changing the amount of your income that is taxable, i.e., your tax withholding. It is advisable to revise it every year and make adjustments in congruence with life changes, for instance, marriage. Filing status is also quite important, and you may choose to continue filing your tax returns as an individual.

Claiming Deductions

Documenting expenses can often help you understand the deductibles you can claim, hence helping to lower your taxable income. If you have any of the documents below, compile them and submit them with your tax return to reduce your tax bill:

Charitable donations: records of all donations (itemized and non-itemized) to 501 (c)(3) registered charities. There is no upper limit on itemized cash donations; for those who claim the standard deduction, the maximum deduction is $300.

Homeownership documents: mortgage payments, property tax statements, moving expense records.

Medical expense records: hospital and doctors’ bills, health insurance payments, Medical Savings Account contributions. Try to itemize all expenditures greater than 7.5% of your adjusted gross income. For HSA’s, contributions up to $3,600 for individuals are tax-deductible.

Child Care expense documents: records of payments such as daycare or caretaker fees.

Educational expense documents: tuition fees payments, student loan payments, expenditure on courses/supplies that improve skills related to your job.

Retirement planning proofs: proofs of contributions made to IRA and 401k accounts. Contributions are up to $6,000 for those younger than 50 are tax-deductible.

State and local income tax payment records: this deduction is capped at $10,000 for any payments toward local and state taxes.

Claiming Credits

Tax credits can help reduce your tax liability as an individual filing tax returns. Using popular credits often results in a lower tax bill and larger refund. Keep the following documents handy:

Letter 6419: Child Tax Credits are worth up to $3,000 per qualifying child above the age of six and up to $3,600 for kids under six.

Form 1116: for claiming foreign income tax credits, i.e., income earned from assets in India.

Adoption documentation: for families with adopted children to claim Adoption Tax Credits.

Proof of financial support provided to a dependent: individuals taking care of dependents without a steady income claim Dependent Tax Credits. This credit significantly reduces liability to offset the costs incurred.

The Bottom Line

There’s nothing like the feeling of calm when confronting something as monstrously overwhelming as tax season. Being organized is the key to being prepared, so make sure to use this checklist to get your documents in order.

If you’re still unsure about the best way to file your returns and which deductions and credits are best suited to your situation, sign up for free with AOTAX today to get your questions answered.

AOTAX’s mission over the last 15+ years has been to help Indian IT professionals in the US. We have a dedicated team to solve all your queries and help you get the most from your tax returns.

Taxpayers should file IRS Form 8962 with their federal income tax return to claim the Premium Tax Credit (PTC). The PTC is intended to assist taxpayers in recouping some of the costs of health insurance purchased through the health insurance marketplace.

Taxpayers reconcile the tax credit they are entitled to with any advance credit payments for the tax year using Form 8962. In addition, to qualify for the PTC, taxpayers or their family members should have been enrolled in a health insurance program through the marketplace for a minimum of one month during the tax year.

The cost of available health insurance, the size of the taxpayer’s family, where the taxpayer lives, and the address determine the tax credit amount. Hence, if you receive healthcare from your employer (1095-C form), you will not file Form 8962. Also, if you have health insurance through another company and have received a 1095-B form confirming your coverage, you cannot use Form 8962.

Given all the terms and conditions regarding the Form, it could get challenging to fill the same. If you’re wondering how to fill out Form 8962, then you’re on the right page.

What Is Advance Premium Tax Credit

The advanced premium tax credit is a federal tax credit for individuals that reduces the monthly health insurance premiums they must pay when purchasing coverage through the Marketplace.

When you sign up for a qualified health plan on the health insurance marketplace, the system determines whether you are eligible for a subsidy. The marketplace determines your eligibility for a subsidy based on your income and personal exemptions, known as an advance payment or APTC.

You should report any changes in your income or personal exemptions to the marketplace if they occur throughout the year. If you do not, you might receive too much or too little in APTC.

On the other hand, if your income increases and you do not declare it, the government may pay you or your insurer too much APTC. In such a case, you use Form 8962 to reconcile your PTC eligibility with the APTC already paid.

If you are qualified for more PTC than you were paid in APTC, you may be able to get the difference you paid back in your tax return.

For 2021 and 2022, the American Rescue Plan Act of 2021 eliminates the advanced premium tax credit income cap. Instead, on the high end, the act caps premiums at 8.5% of the payer’s modified adjusted gross income (i.e., for people with adjusted gross income above 400% of the poverty level).

The “net Premium Tax Credits” are also claimed using Form 8962. These are for qualified persons who, instead of receiving an APTC, choose to pay their insurance premiums out of pocket throughout the year and then claim the PTC at the end of the year.

Points to Consider Before Filling Out Form 8962

These are some things you should consider before starting the filing procedure. This checklist will help you keep track of the validity and authenticity of your filing process:

Either you or a member of your family must be enrolled in a health plan covered by the “Market Plan”.

As a recipient, you are lawfully residing in the US. This is to establish residency.

To complete the filing of Form 8962, an extra Form 1095-A is necessary.

The marketplace sends this, and if you haven’t received it by early February, you have to contact them.

The PTC estimate provided by the Marketplace is likely to decide your Advance PTC eligibility.

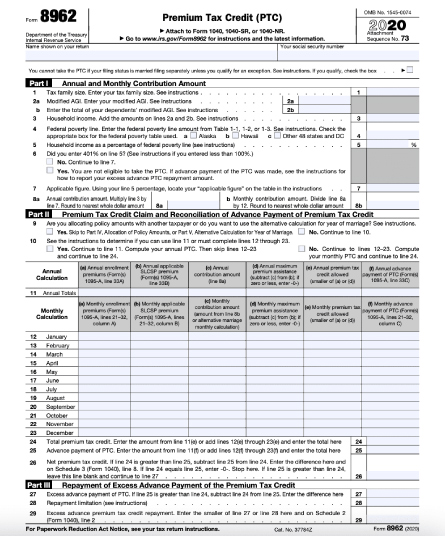

Reading Form 8962

Form 8962 is a two-page document with five sections:

Part I is where you enter the annual and monthly payment amounts based on the size of your family, modified adjusted gross income, and household income.

Part II is where you balance the amount of your advanced premium tax credit with the amount of your monthly premiums.

Based on the information you supplied in Part II, Part III is utilized to determine any excess advance premium tax credit payments.

Part IV permits you to assign policy funds, whereas Part V is utilized for alternative calculation of your year of marriage.

To complete each component of the form, you’ll need Form 1095-A, as well as your Form 1040, which shows your modified adjusted gross income.

If the information on your Form 1095-A is incorrect, you must update it before filling out Form 8962. Contact the Health Insurance Marketplace to receive an updated form.

Download the Premium Tax Credit (Form 8962)

The IRS website has Form 8962, which is free to download. When you move through the program’s questionnaire format, this form should be generated for you if you’re filing taxes electronically.

Instructions for IRS Form 8962: A Complete Guide

If you’re unsure how to fill out Form 8962, follow the steps below to learn everything you need to know:

Step 1

First, you’ll need to obtain IRS Form 8962. You can get it from:

The Treasury Department

IRS website

Step 2

You will receive a PDF file of the form. Now, you will begin the filing procedure.

Fill in your name as it appears on your tax return and your Social Security number at the top of the form.

Step 3

Next, go to “Part 1” of the form. Begin by filling in the exemptions from Form 1040-A on the first line. Next, you should enter the amounts relating to the updated AGI on lines 2A and 2B. Next, you must add the Household Income to line 3; to do so, simply add the numbers from lines 2A and 2B. To complete line 4, simply select the appropriate option and enter the proper value. Finally, add the household income in terms of the percentage of the Poverty Line on line 5. Skip to line 7 if your value is more significant than 401%.

Step 4

In Line 7, enter the needed figure, and then in Line 8, enter the annual contribution amount.

Step 5

Now, we’ll go to Part 2 of IRS Form 8962. The name of this section is: “Premium Tax Credit Claim and Reconciliation of Advance Payment of Premium Tax Credit.” Proceed to Line 11 after selecting the proper options on Lines 9 and 10. There’s a little table to fill up the monthly amounts column-by-column. You’ll fill up the lines 12-23 due to this. Line 24 (Total PTC) is below the table and is where you must add the Total PTC. Then comes Line 25, where you must enter the Advance payment.

Step 6

We shall not continue to Part 3 of the application. This section is known as “Repayment of Excess Advance Payment of the Premium Tax Credit.” So instead, we’ll go on to Line 27, where you’ll need to fill in the ‘Advance Premium Tax Credit.’

Step 7

This section is known as “Shared Policy Allocation.” Lines 30-33 make up this section. You must fill in the values in the table that is provided, which includes:

The policy number is entered in the field a.

SSN field (field b).

In Field c, enter the allotment for the first month.

Fill in the allotment ending the month in Field d.

The premium % should be entered in field e.

In field f, enter the SLCSP percentage.

In field g, enter the advance payment for the PTC percentage.

Step 8

This section is the “Alternative Calculation for the Year of Marriage”. Add the alternate entries for your Social Security Number in fields a, b, c, and d when you get to line 35. Then, add the alternate entries for your spouse’s SSN on fields a, b, c, and d when you get to line 36.

Final Thoughts

Whether you receive an Advance PTC or claim a PTC at year’s end, you must file Form 8962 with your tax return if you purchase health insurance through the Marketplace and qualify for Premium Tax Credits (PTC). In addition, your local health exchange should send you a Health Insurance Marketplace Statement (Form 1095-A) to assist you in filling it out.

Are you wondering how to fill out Form 8962?AOTAX makes preparing and filing your taxes quick, easy, and affordable so that you get your maximum refund.

We are Registered Tax Agents with vast hands-on expertise, and we take great pride in assisting our clients in achieving their objectives. Thanks to a team of highly skilled and experienced Tax Accountants, we do everything we can to reduce your tax liability while making the overall taxation process as efficient, simple, and cost-effective as possible. Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

To file a yearly tax return is unavoidable for millions of people in the United States. However, the IRS granted everyone until July to file their tax returns last year because of the COVID-19 pandemic. Since no such extension has been offered this year, you will have until April 15 to submit your forms.

However, just because you have the option of filing later does not mean you should. To file early this year, you must do it in February. In February, the IRS will accept returns for the 2021 tax year.

Early filing can result in a more accurate return, more time to pay a tax payment, and a lower risk of identity theft related to taxes. In addition, there is no reason to wait for individuals with simple tax returns.

This article will see why claiming tax returns early on is beneficial and how can AOTAX help Indians working in the US.

Why File Taxes Early?

Although many taxpayers file their tax returns on or before April 15 each year, there is no need to put it off until the last minute. Indeed, submitting your tax return early can make sense for several reasons, including obtaining your refund faster and reducing your risk of identity theft.

Even if you don’t file early, there are compelling reasons to start your tax planning as soon as possible. For example, it offers you the time you need to gather the documents and information you’ll need to claim all of your deductions—avoiding the stress of rushing for receipts at the last minute.

The Benefits of Filing Taxes Early

There are several advantages to filing tax returns early instead of waiting until Tax Day:

1. File early for a faster refund

You may prevent procrastination, get peace of mind, and cross this critical item off your new year’s to-do list by filing early. So, why not submit yours once the IRS announces that it will begin processing returns?

The IRS issued refunds to 129.8 million filers for the 2020 filing season, averaging $2,815 per refund.There’s no reason to let the government keep your money for any longer than necessary if you have money flowing to you. In addition, because the IRS will not be as busy early in the tax season as it would be in April, filing sooner means a faster refund.

Some people rely on their tax refunds to cover significant expenses. If you file early, you’ll get the money sooner and avoid having to take out an expensive short-term loan to meet those charges, which is especially important if you’re still paying off your holiday obligations.

2. File early to avoid identity theft

The sooner you file, the less time a fraudster has to file in your name and steal your money. This can cause havoc, especially if the fraudster claims bogus deductions, fails to declare income, or otherwise taints a tax return filed in your name.

It might take months to clean up a mess like this. Unfortunately, you may not realize you’ve been a victim of identity theft until the IRS alerts you to a potential problem with your tax return. The IRS warns that you should be on the lookout for tax-related identity theft if:

According to IRS records, you have to pay money for an employer you did not work for.

Due to a duplicate Social Security number, you cannot e-file your tax return.

When you haven’t taken any action, you receive an IRS notice that your current online account has been accessed or disabled.

You get a notice from the IRS that an online account in your name has been created (and you did not make it.

You receive a letter from the Internal Revenue Service (IRS) inquiring about an unfiled tax return that appears suspicious.

You get a tax transcript in the mail even though you didn’t ask for it.

You receive notification from the IRS that you owe extra tax or that your refund has been offset, or that measures have been taken against you for a year in which you did not file a tax return.

Filing early allows you to fully comprehend any changes in tax legislation and deal with life situations that may affect your filing status. Last-minute mistakes can result in audits, resulting in penalties and interest. This premise is more essential than ever, given the Tax Cuts and Jobs Act (TCJA).

Your certified public accountant (CPA) or other tax preparers will be less busy than in April in January and February. Early access implies your CPA will have more time to properly analyze your case and assist you with your tax return.

You will need information from your most recent tax return, whether you’re purchasing a house or going back to school (and applying for financial aid). You will have the most up-to-date information if you prepare your taxes early.

4. Avoiding amended returns

You’ll have more time to file a correct return if you start early. An incorrect return will most certainly be rectified. Audits are more likely to occur when returns are amended.

Here are some things to keep in mind as you strive for precision:

Official documents contain errors. W-2s, 1099s, interest statements, and anything else used to substantiate a deduction should all be checked. In addition, mistakes are made by businesses, banks, and financial organizations. Before you file, ensure you correct any such errors.

Early filing may result in the loss of essential documents, such as a 1099 or K-1 that arrives late. Therefore, double-check that you have all the necessary documents before clicking “submit” or dropping your return in the mail.

Amendments that are not complete. If you have to change your return, don’t just fix the parts that benefit you. Anything incorrect should be corrected.

Changes to tax forms. Form 1040 has changed due to the Tax Cut and Jobs Act (TCJA) of 2017. If you previously filed Forms 1040-EZ or 1040-A, you will no longer be able to do so. If you’re above the age of 65, you can now use the new 1040-SR “U.S. Tax Return for Seniors”.

Legislation enacted before April 15 may not be implemented into paper tax forms or outdated tax software. So keep an eye on the news. Also, keep an eye out for any alterations that may have gone unnoticed. You can file an updated return if necessary.

5. Time to save

If you owe the IRS money, filing early provides you more time to save. However, even if you owe the IRS money, there may be a compelling reason to file your tax return right away.

You don’t have to pay any taxes you owe until the filing deadline if you file your return in the middle of January. However, if you prepare your Form 1040 ahead of time, you will have more time to coordinate your payment.

In addition, those that need to calculate out how much they will owe the IRS will benefit from the extra time.

Waiting to find out you owe more than you anticipated could put a strain on your finances. So, to avoid an unexpected tax bill, the IRS recommends monitoring your withholding and tax payments in the fourth quarter of the year.

6. Avoiding a tax extension

If you file your tax return early, you may not need to file an extension. Rather than being a financial need, time extensions are frequently required owing to disorganization.

Some people who wait until the last minute to file their taxes simply need more time to hunt for more deductions or gather receipts.

If you rush the process too close to the deadline, you’ll almost certainly need the assistance of a tax professional to help you organize your finances and file your return.

Even worse, if you file an extension but don’t pay what you owe if there is a balance owing, the IRS will charge you interest and penalties on the unpaid tax bill until it is paid in full.

What Happens If You File Your Taxes Late?

Most people have until April 15 to file their federal income tax returns and pay any taxes they owe. However, the IRS is authorized by law to impose penalties on taxpayers who fail to file a tax return or pay taxes owed by the due date. In the absence of reasonable cause, a failure to file a penalty is assessed on returns filed after the deadline or extended deadline.

What are the consequences of filing taxes late?

Is a penalty imposed by the Internal Revenue Service for not filing taxes on time? Yes, there is:

For each month or part of a month that your return is late, the combined penalty is 5% (4.5% late filing and 0.5% late payment), up to a maximum of 25%.

The late filing penalty is imposed on taxes that are not paid by the due date. Therefore, the total tax displayed on your return fewer amounts paid through withholding, estimated tax payments, and allowable refundable credits equals unpaid tax.

If you still haven’t paid after five months, the failure to file a penalty will be increased to 25%; however, the failure to pay fine will remain in effect until the tax is paid.

Failure to file and pay results in a total penalty of 47.5% of the tax (22.5% late filing and 25% late payment).

If your return is more than 60-days late, the minimum penalty is the lesser of $435 or 100% of the tax that must be declared on the return.

The Bottom Line

Many people wait until the last possible moment to file their federal income tax returns every year. Despite this tendency, there are several reasons to file your taxes as soon as feasible.

You should file your return as quickly as possible if you are eligible for a refund. There are additional benefits to filing early for individuals who owe a balance.

Are you looking at filing your taxes early? Then, AOTAX can relieve you of this burden by filing your Tax Returns for you.

We are Registered Tax Agents with vast hands-on expertise, and we take great pride in assisting our clients in achieving their objectives. Thanks to a team of highly skilled and experienced Tax Accountants, we do everything we can to reduce your tax liability while making the overall taxation process as efficient, simple, and cost-effective as possible.

The person you refer and who pays taxes through our services is also eligible for this referral bonus. This bonus amount can be used to deliver their tax services or exchanged for an Amazon gift card.Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

An IT job in the US comes with an H1B visa and income in dollars. But it soon loses its charm when it comes down to income tax filing. As per estimates, H1B visa holders nearly pay 35% – 40% of their gross income as various taxes – federal, state, and local. (How much tax do H-1B holders pay? – Greedhead.net) Hence, to cut down your losses and maximize your savings, it is important to have a tax planner by your side that will help you be tax compliant and reduce the tax burden.

While filing your income tax returns (ITR), you can choose between a tax preparer and a tax planner (advisor). A tax preparer will help you with your immediate income tax filing. While a tax planner can help you with your taxes in the long run.

Job of a tax planner:

Everyone has financial aspirations they strive to achieve for themselves and their family. Some want to buy a house, save for retirement, children’s education, or build assets to enjoy during their sunset years. An efficient tax planner understands these goals, analyses their feasibility, and draws out a financial plan to achieve them. They ensure that you fulfill your ambitions without defaulting on your tax payments with the Internal Revenue Service (IRS). They help reduce your tax liability, maximize your tax credits and build wealth accordingly. If you hire a good tax planner you can build assets that you and your family can enjoy.

Qualification:

A tax planner is an expert in their field and knows taxation laws. They are aware about the latest tax laws and procedures. They are also Certified Public Accountants (CPA) in general tax planning or is a specialist in a specific area of tax laws. They are not subject to any state or federal regulations.

Services A Tax Planner Offer

Apart from income tax filing, a tax planner offers you the following services:

They provide financial advice to reduce your tax burden in the years ahead.

They advise on how to maximize your income with appropriate tax savings.

They give advice on financial issues like buying a home, retirement savings, etc., which will help you save taxes.

They help when you get in trouble with the IRS over a tax issue.

Six Steps To Choose A Tax Planner For Income Tax Filing

By now, you have an idea of your financial goals. Now its time for you to choose a tax planner who helps you achieve all this without breaking a sweat. Here is a fool-proof 7 step plan to choosing a tax planner:

1) References: Choosing the right tax planner is essential to have a smooth income tax filing experience. It also makes your life hassle-free all year-round instead of just January-April. The easiest way to find the right tax planner is to ask friends and relatives. You can ask your H1B visa-holder colleagues to give you some references.

2) Check credentials: Once you have found a planner you think is right for you, ask them for some references and credentials.

3) Experience & expertise: Relevant experience matters when you are caught on the wrong side of the taxation laws. Look for a planner whose resume has the number of years they spent in the field managing the IRS. Find someone whose specialty is handling niche clients. For instance, AOTAX has spent 15 years helping over 2 lac Indian H1B visa holders plan and file their income taxes. They are a team of tax planners and advisors who have helped their clients maximize their tax savings.

4) Multi-tasker: Look for someone who can not only be your trusted financial advisor but also a tax preparer. They will help you create wealth as well as file your ITR on time.

5) Check for complaints: This step is important and saves you a lot of time. Check with the Better Business Bureau if there are any complaints of fraud against the advisor if they are also a tax preparer. You can even check with the American Institute of Certified Public Accountants (AICP) if the tax planner/advisor is being investigated for any complaints.

6) Fees: Be clear about the fees you will pay them for their services. Most planners charge a percentage of your asset in question.

7) Ethics: Being ethical is important when you pay your taxes. If a tax planner suggests dubious ways to save tax then that isn’t right. If they suggest to over or under-report your income, claims dependents when you are not eligible, that is a red flag.

With these steps, it is possible for you to easily hire the best tax planner and pay your dues. Plus you can also make the most from your current income.

If you are an H1B visa-holder from India looking to file your income tax returns in the US while saving some extra dollars, do get in touch with us on AOTAX.com. Our team of expert tax planners can easily meet your financial goals. Recommended: What Makes AOTAX the Most Preferred Tax Assistant in 2022

With the golden ticket of H1B visa comes the clear path toward the American Dream. And of course, with the American Dream comes the American Reality—the brick-and-mortar behind-the-scenes that go towards building a life in the USA.

Tax returns are very much a part of this reality, and while reaping the system’s benefits may be smooth-wading through, the paperwork at the end of it is not.

However, filing your tax returns doesn’t have to be all drudgery and doom. Being organized is critical, and we help you out below with an extensive list of all the possible documents and forms you may need to file individual income tax returns.

Who Qualifies for Tax Returns in the US

However, before diving in, let’s quickly look at who exactly qualifies for paying taxes and receiving the returns that come with it.

To refresh, any individual who meets the ‘Green Card Test’ or the ‘Substantial Presence Test’ is considered a resident alien and thereby is liable to pay taxes in the same manner as any US citizen.

Here’s a breakdown of the two tests:

The Green Card Test—if you have not renounced your alien registration card (a green card), and neither has your privilege of immigrant status been terminated by the USCIS or a federal court, you pass the Green Card Test.

The Substantial Presence Test—you pass the SPT if you have been residing in the US for at least 31-days of the current year and 183-days total over the current year and the two years preceding it. More specifically, this count must include all days in the current year, one-third of the days present in the year before the current year, and one-sixth of the days present two years before the current year.

Now, let’s look at precisely what you need to file a complete and accurate tax return. To make things easy, we’ve grouped the documents according to their function.

Personal Information and Dependent Information

Basic information forms the crux of tax returns in the US, so it is essential to keep the following documents handy:

Previous tax returns and statements for reference.

Social Security or Tax ID numbers for both you and your dependents, if any.

Income-Related Documents

Furnishing proofs of earnings is an integral part of filing your taxes. As an Indian professional residing in the US, it is important to note that you are liable to declare your global income (from every source) in your tax returns.

That means earnings on mutual fund dividends, interest earned on stocks, bank deposits, and fixed deposits, among others, are all taxable. Below is a list of documents you may require while filing:

W-2 forms from employers.

Form 1040 to declare taxes paid in previous years and to declare foreign income.

Form 1099 series, each ending with a different suffix for different revenues earned. For instance:

1099-INT (interest income)

1099-G (government payments and tax refunds)

1099-K and 1099-MISC (freelance gig payments)

1099-R (pension income)

1099-S (stock sale income)

1099-B (property sale income)

1099-DIV (dividends)

1099-SSA (Social Security benefits)

Form 1095-A for Health Insurance Marketplace Statements.

Records of cryptocurrency transactions and interest earned.

Expense records such as bank or credit card statements.

Compiling the applicable documents below could help reduce the taxes you pay:

Records of donations to charity.

Homeownership documents such as mortgage payments and property tax statements.

Medical expense statements such as hospital and doctors bills and health insurance payments.

Childcare and educational expenses include daycare fee payments and tuition fees or loan payments.

Proofs of retirement account contributions.

Records of state and local income taxes paid.

Documentation for Credits

Tax credits are as valuable as deductions and help reduce your tax liability. It is important to have the necessary documentation in your tax return to claim these.

Here are some of the most common tax credits you can claim:

Child Tax Credits that are worth up to $3600 per child. Hold on to Letter 6419 for the same.

For foreign income tax credits, fill in and attach Form 1116 to your return to reduce the brunt of taxes paid on income earned back in India.

Adoption Tax Credits for families that have adopted children.

Dependent Tax Credits in case you are supporting a dependent while unemployed yourself. This credit reduces liability to offset the cost of paying for a dependent without a steady income.

Income Adjustments and Declarations

With personal and financial changes such as job changes, getting married, or having children, it is advisable to reconsider your withholding.

In a country with regulations far different from what we’re used to in India, preparing for tax season is taxing, saying the least. However, organizing your receipts, statements, and forms is an excellent first step to take.

However, filing on your own without knowing how to claim credits or deductions or whether you’re even eligible for them is doing a great disservice to your bank balance.

AOTAX has been helping Indian IT professionals in the US for more than 15-years and is well-versed in the challenges you face and how to get the best returns in your situation. Let us help you with our planning, advisory, and consulting services to ensure you only have to enjoy the American Dream while we take care of the American Reality. Sign up for free today to get a feel for how we work and what we can do for you.

Recent Comments